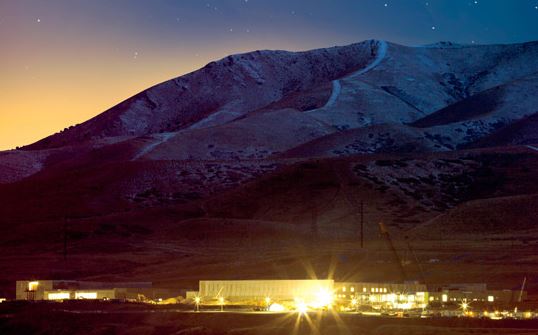

Revelations that the Government is collecting millions of phone records and digital communications stored by major Internet services should come as no surprise. The Government is building a data center in Bluffdale, Utah that is five times larger than the U.S. Capitol. The problem is that information can be misinterpreted that may unfairly stereotypes people and may be possible someone might be classified as a potential risk simply for buying products commonly used.

Revelations that the Government is collecting millions of phone records and digital communications stored by major Internet services should come as no surprise. The Government is building a data center in Bluffdale, Utah that is five times larger than the U.S. Capitol. The problem is that information can be misinterpreted that may unfairly stereotypes people and may be possible someone might be classified as a potential risk simply for buying products commonly used.

The same holds true for State Health Insurance Exchanges being created under the Affordable Care Act. Big medical information data warehouses have existed for decades.

Many consumers are surprised to learn of the existence of a reporting agency for the health industry, the Medical Information Bureau (MIB). Two other large medical data collection agencies include IntelliScript (Milliman) and MedPoint (Ingenix). All three companies will very likely have data minded records on all prescription drugs you have purchased over the past five or more years. This data is often used by life insurance or disability insurance companies to determine whether or not to sell you insurance.

According to its website, MIB Group, Inc. is a member-owned corporation that has operated on a not-for-profit basis in the United States and Canada since 1902. MIB’s Underwriting Services are used exclusively by MIB’s member life and health insurance companies to assess an individual’s risk and eligibility during the underwriting of life, health, disability income, critical illness, and long-term care insurance policies.

What Information does the MIB Collect? The MIB does not collect copies of actual medical records. Rather, members report information to MIB using highly confidential codes that signify different medical conditions. These are conditions can have a significant impact on an applicant’s health. Medical codes may include the following:

- Credit information

- Medical conditions

- Medical tests and results

- Habits such as smoking, overeating, gambling, drugs

- Hazardous avocations and hobbies

- Motor vehicle reports (poor driving history and accidents)

In theory, MIB data is used to prevent fraud, potentially identifying those who attempt to hide known medical conditions when applying for insurance and insurers using MIB data cannot use the information obtained as the basis for denying insurance. However, those medical codes can be used during insurance premium classification. Thus, your insurance rate will be higher or lower depending upon “Rules Engine” calculation.

MIB, IntelleScript and MedPoint codes are commonly feed into insurance “Rules Engines.” In Health Insurance Exchanges, Rules Engine for Eligibility & Enrollment will maintain the “rules repository” for calculation of premiums and for eligibility determination and enrollment. It allows processing of individual & household information and calculates premium amount and eligibility results.

To handle the sheer number of applicants, rules-based core systems will be mandatory when Health Insurance Exchanges open. But each system has a life of their own and creates problems when improperly governed. The amount of data exchanged between federal and state agencies is tremendous and proper management and maintenance is critical.

For individuals and families using a State Health Insurance Exchange, will MIB information be used to set premiums? Will “rules” engines calculate premiums so high that it makes the premium impossible to pay? Hard to say, for one cannot find an easy answer at the moment.

1 Trackback or Pingback for this entry:

[…] Revelations that the Government is collecting millions of phone records and digital communications stored by major Internet services should come as no surprise. The Government is building a data ce… […]